Ever since the establishment of BharatPe in 2018, it has excelled tremendously in the fintech sector. The cause? You may ask. The key reason is charging zero fees on digital payment systems! As you know BharatPe is a QR-based payment app specially designed to make payments free for all of its users. It has numerous advantageous features like free UPI payments, Bharat Swipe (POS card acceptance machine), merchant loans, digital gold, and a 12% club.

Out of these, the 12% club is thriving well in the market. Being a rookie investor or a customer, your mind must be quizzed with lots of questions like what exactly a 12% club is, whether to use the 12% club, whether it is good enough or not, whether it is safe, and so on. So, in this article, you will get a thorough explanation of 12% club– a BharatPe product.

WHAT IS A 12% CLUB?

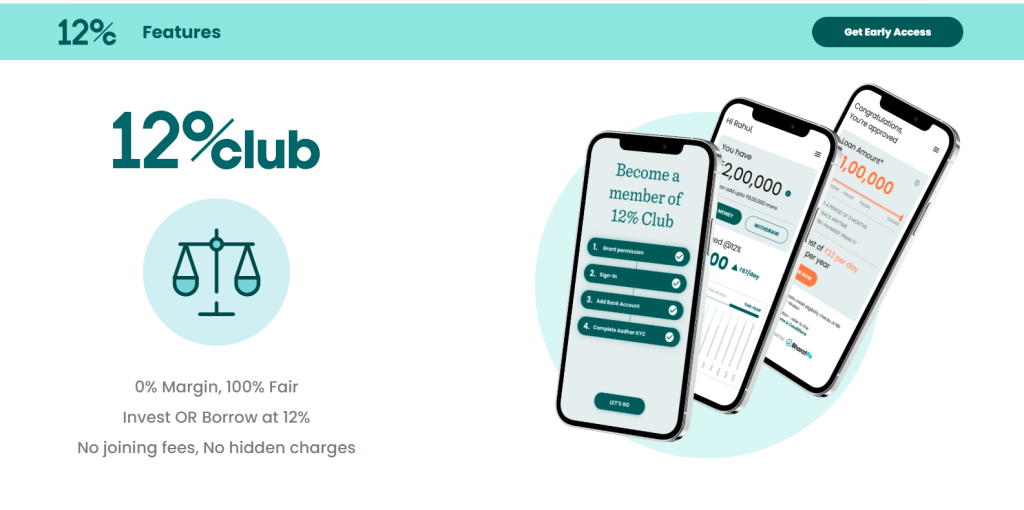

In August 2021, BharatPe launched its first peer-to-peer lending app called “12% Club.” BharatPe partnered with the NBFCs that are approved by RBI to offer this fintech innovative investment-cum-borrowing product for merchants and consumers. You can download the 12% club app from Google Play Store or Apple App Store. You can enjoy numerous alluring features of this app. Such as-

- You can invest and earn up to 12% of annual interest or borrow at a similar rate. (Hence, it acquired the name 12% club). And that too without any lock-in period. To use it, you can simply invest your savings anytime by selecting the “lend money” option through BharatPe’s partner P2P NBFCs.

- You can also avail of loans of up to INR 10,00,000 (10 Lacs) without any collaterals for a period of 3 months.

- This platform will not charge any processing fees or prepayment fees for your loans.

- You can start the investments with the least amount of INR 1000.00 while receiving credit of interest on a daily basis.

- Similarly, you can also withdraw your investments completely or partially whenever you want without paying any withdrawal charges.

Note: Peer-to-peer lending (P2P lending) is an alternative method of financing where you can obtain loans directly from other individuals (peers) without the need for any financial institution or middlemen. 12% club is one such P2P financing app.

How does the 12% club work?

Fundamentally, the 12% club app works on P2P lending financial technology. It allows users to lend or borrow money from one another (among peers) without going to a middleman or a bank. So, this app connects the borrowers directly to the investors or lenders. It involves the following basic steps-

- Step 1: An investor or lender opens an account in the 12% club and deposits a specific amount of money to be disseminated in loans.

- Step 2: On the other hand, the loan applicant or borrower posts a financial profile and the rate of interest he is willing to pay. Usually, the competitive rate of interest in this app is 12%.

- Step 3: The loan applicant (borrower) goes through various offers given by the lenders, reviews them, and accepts one of them. They can borrow up to 10 lacs without any collaterals (for 3 months) and processing fees. In case, if you want to borrow a large amount, then you can break your requests into chunks and accept multiple offers simultaneously.

- Step 4: All the money transfers and payments occur automatically on this platform.

Thus, you can earn up to 12% interest on your money or borrow money with 12% interest.

Is the 12% club safe and approved by the RBI?

To ensure safety, this app has made KYC mandatory for all of its users. It is compulsory to link your bank account and validate your Aadhaar using OTP, submit your photograph, complete your KYC, and lastly, agree to all the terms and conditions to authorize your account on the 12% club app.

As far as your concern on the 12% club’s authenticity concerning RBI, it has partnered with various NBFCs (Non-Banking Financial Institutions) that are approved by RBI. Some of those NBFCs are-

- Hindon Mercantile Limited

- LendenClub (Innofin Solutions Private Limited)

- LiquiLoans (NDX P2P Private Limited)

As you know, every investment is associated with risks in one form or the other. No investment occurs in a safe haven. However, the 12% club app ensures you 12% returns on your investments for sure.

How does the 12% club make money?

The revenue model of the 12% club is based on P2P lending. Eventually, the services of the “12% club” are fueled by standard NBFCs to give loans to customers. They charge a small amount of money from the NBFCs while providing loans or credits to customers/users. The NBFCs of 12% club include Hindon Mercantile or LendenClub. Other than this, the 12% club is also flooded with monthly investments worth USD 5 million. Individual investors and loan disbursals are the key players in the investments. The referrals and more than 2500 downloads have hugely contributed to the growth of this app.

Overall Public feedback on the 12% club so far?

The 12% club has struck the perfect chord with a diverse set of digitally savvy customers. They range from salaried individuals to investors and professionals with disposable incomes who want to fund various financial instruments. A lot of people are doubtful about investing through this. Despite some risks associated with it, this fintech product of BharatPe has been well-received in the market. It is a good option for those who seek high yields and returns while parking their money. Also, it is beneficial of investors who have a high risk appetite. Thus, this peer-to-peer lending/borrowing app is playing a key role in driving financial inclusion in the nation.

Disclaimer: Borrowers defaulting is one of the biggest risks with P2P lending but, thankfully, reputable companies plan for this outcome. We do not endorse using this product. Use it at your own discretion.